Income From House Property: A Guide To The Tax Payer

In India, if you own a house and it generates revenue in the form of rent or in any other form, then it falls under income from house property. As per the Income Tax Act 1961 if you own any house property and it generates revenue for you then it is a taxable income.

Now, whether you rent your house or not, and even if your self-occupied house do not generate any income then also you have to pay taxes for your house. In this article, you will also know how you can reduce your tax liability within yourself.

You may have to pay taxes from your income from House Property but still, there is scope to get the tax deduction under certain conditions.

Table of Contents

- What Is Income From House Property?

- What Constitutes Income from House Property?

- What Is Taxable As Income From House Property? Annual Value Of Property

- Income Tax Regime From Section 22-27

- Methods For Determining Annual Value From Income From House Property

- What Makes Rent Taxable In India?

- Calculating Income From House Property

- House Property Income Calculation Chart

- Deduction In Respect To House Property Where Annual Value Is Nil

- Final Take Awa

What Is Income From House Property?

Income from house property refers to the earnings or revenue generated from a residential or commercial property that you own. In the context of taxation, particularly under the Indian Income Tax Act (though the concept applies similarly in many jurisdictions), it is a specific head of income that deals with the income derived from renting out or owning a property. Here’s a breakdown:

What Constitutes Income from House Property?

- Rental Income: The most common form is the rent received from letting out a property, such as a house, apartment, or commercial space.

- Annual Value of Self-Occupied Property: Even if a property isn’t rented out (e.g., you live in it), tax laws may assign a notional income based on its “annual value” in some cases, though this is often exempt or treated differently depending on the jurisdiction.

- Co-owned Property: If you co-own a property, your share of the income from it is considered.

What Is Taxable As Income From House Property? Annual Value Of Property

Tax on House property is not calculated based on actual rent received. There are also some of the other aspects that you need to consider before arriving at income from house property. You must also consider the fact that tax is calculated on the basis of the annual value of the property. In most cases, it is an estimated value that the property can generate from the market every year.

There are certain points that you need to consider before determining the income from house property. Some of its key points that you should know here are as follows:-

- Size and Amenities: Depending on the size of the property and the amenities it offers the annual value of the property gets determined.

- Location:- If your property is located in the prime location of the city then it creates higher rent and thus leads to higher annual value.

- Municipal Taxes:- If you pay taxes to the local body owners then also it is added to the annual value.

- Age & Condition: Old properties have a lower annual value as it need renovations all the time.

Why traditional? Choose a 90% Practical BBA Degree1-year paid internship + 10 Simulation Software + 4 Certifications that employers are looking for |

|

| BBA in Finance and Accounting |

Classification Of House Property

Under the Income Tax Act, 1961 (Sections 22 to 27), income from house property refers to any income earned from a building or land attached to it, such as residential houses, commercial buildings, shops, offices, or related facilities like parking areas. It does not cover vacant land without a building or properties used for the owner’s own business or profession.

For taxation purposes, house properties are classified into three main categories based on how the property is used and whether it is occupied or rented out:

1. Self Occupied Property

This is a property that the owner uses for their own residence or for the residence of their family members. It also includes a property that remains vacant because the owner is living elsewhere due to employment or business reasons (and is treated as self-occupied).

The gross annual value of such property is taken as nil, meaning no rental income is taxed on it. Since FY 2019-20, an individual can treat up to two properties as self-occupied. A key benefit is that interest paid on a home loan for these properties is deductible up to ₹2 lakh in total per year under Section 24(b).

2. Let Out Property

This refers to a property that is actually rented out to tenants, either fully or partially, during the financial year. Here, the income is fully taxable. The gross annual value is calculated as the higher of the expected fair rent (based on municipal value or similar properties) or the actual rent received (after adjusting for any vacancies or unrealized rent).

Deductions available include municipal taxes paid by the owner, a standard 30% deduction on the net annual value, and the full interest paid on any borrowed capital (home loan) with no upper limit.

3. Deemed Let Out Property

This applies to properties that are owned by the taxpayer but are neither self-occupied nor actually rented out (for example, vacant properties or additional houses beyond the two allowed as self-occupied).

Such properties are treated as if they were let out, even if no rent is received. The gross annual value is determined in the same way as for let-out properties—based on the expected or fair market rent. The same deductions as for let-out properties apply, including the 30% standard deduction and unlimited home loan interest.

Income Tax Regime From Section 22-27

Sections 22 to 27 of the Indian Income Tax Act, 1961 form the legal framework for taxing Income from House Property in India. These sections outline what qualifies, how it’s calculated, and the deductions available. Let me break it down clearly based on this regime, as applicable up to April 06, 2025, reflecting the latest known provisions.

| Section | Application Of Taxation |

|---|---|

| Section 22 | Defines the changeability of income from house property. |

| Section 23 | Explains how to determine the Annual Value of the property. |

| Section 24 | Specifies deductions available from the Annual Value. |

| Section 25 | Deals with amounts not deductible (e.g., unrealized rent rules). |

| Section 25A | Addresses unrealized rent recovered later. |

| Section 26 | Covers property owned by co-owners. |

| Section 27 | Defines “owner” and related terms. |

These are some of the basic concepts of House property that you should be well aware of. Income from house property can offer a clear guide to the taxpayers.

Few Accounting related topics for your knowledge

Methods For Determining Annual Value From Income From House Property

The method of the annual value calculator depends on its uses. So, you must get through the concepts to have a better idea of it.

1. Let-Out Property (Actually Rented Out)

For properties rented out for the whole or part of the year, GAV is determined as follows:

-

Step 1: Compare Actual Rent and Expected Rent:

-

Actual Rent Received or Receivable: The total rent collected or due from the tenant for the year.

- Adjusted for unrealized rent (rent not collected, but only deductible if unrecoverable under conditions in Section 25A—e.g., tenant vacated, legal action taken).

-

Expected Rent: The reasonable rent the property could fetch, calculated as the higher of:

- Municipal Valuation: The value assigned by local authorities for property tax.

- Fair Rental Value (FRV): Market rent for similar properties in the same locality.

- But capped by Standard Rent (if applicable under Rent Control Acts).

-

-

Step 2: Determine GAV( Gross Annual Value):

- GAV = Higher of Actual Rent or Expected Rent, unless:

- Actual rent is lower due to vacancy (property unrented for part of the year despite efforts to let it out), then GAV = Actual Rent.

- GAV = Higher of Actual Rent or Expected Rent, unless:

-

Example:

- Municipal value: ₹3,00,000/year.

- Fair rent: ₹3,20,000/year.

- Standard rent: ₹3,10,000/year.

- Actual rent: ₹3,50,000/year.

- Expected Rent = ₹3,10,000 (higher of municipal/fair, capped by standard).

- GAV = ₹3,50,000 (actual rent is higher).

2. Self-Occupied Property

For properties used by the owner for residence:

- GAV = Nil:

- Up to two properties can be designated as self-occupied (as per current rules). The GAV for these is zero.

- If you own more than two properties, only two can be self-occupied; the rest are treated as deemed let-out.

-

Example:

- You own one house and live in it. GAV = ₹0.

3. Deemed Let-Out Property

For properties not rented out and not self-occupied (e.g., a second home kept vacant):

-

GAV = Expected Rent:

- Calculated as the higher of:

- Municipal Valuation.

- Fair Rental Value.

- Capped by Standard Rent (if applicable).

- No actual rent is considered since it’s not let out.

- Calculated as the higher of:

-

Example:

- Municipal value: ₹4,00,000/year.

- Fair rent: ₹4,50,000/year.

- Standard rent: ₹4,30,000/year.

- GAV = ₹4,30,000 (higher of municipal/fair, capped by standard).

4. Property Partly Let-Out and Partly Self-Occupied

If a property is used partly for residence and partly rented out:

-

GAV is apportioned:

- Self-Occupied Portion: GAV = Nil.

- Let-Out Portion: GAV = Higher of Actual Rent or Expected Rent for that portion.

-

Example:

- House with 2 floors: 1 self-occupied, 1 rented.

- Total municipal value: ₹2,00,000/year.

- Actual rent for let-out floor: ₹1,20,000/year.

- Expected rent for let-out floor: ₹1,00,000/year.

- GAV = ₹0 (self-occupied) + ₹1,20,000 (let-out) = ₹1,20,000.

5. Property Vacant For Part Of The Year

If a let-out property is vacant for part of the year:

-

GAV Adjustment:

- If vacancy is unavoidable (e.g., tenant left, and you tried to re-let), GAV = Actual Rent for the period it was occupied.

- If no effort to let out, GAV = Expected Rent for the full year.

-

Example:

- Expected rent: ₹3,00,000/year.

- Actual rent: ₹2,00,000 (occupied 8 months).

- GAV = ₹2,00,000 (if vacancy was unavoidable).

Points To Remember While Calculating Home Loan Deductions

Home loan deductions primarily come under two sections: Section 24(b) for interest paid and Section 80C for principal repayment. These are available only under the old tax regime. The new tax regime (default since FY 2023-24) generally does not allow these, except for interest on let-out properties.

- Deductions under Section 80C and Section 24(b) for self-occupied properties are not available in the new tax regime.

- You must explicitly opt for the old tax regime to claim them (possible while filing ITR, except for those with business income).

- For let-out/rented properties, interest deduction under Section 24(b) is allowed even in the new regime (full amount, no cap, but loss set-off rules apply).

- Up to ₹1.5 lakh per financial year (combined with other 80C investments like PPF, ELSS, life insurance).

- Includes stamp duty and registration charges (claimed in the year paid).

- Available only if the loan is from specified lenders (banks, housing finance companies, employer – not from friends/relatives).

- Property must not be sold within 5 years of possession; otherwise, deductions claimed are added back to income.

- Joint loan: Each co-owner/co-borrower can claim up to ₹1.5 lakh separately if they are co-owners.

What Makes Rent Taxable In India?

- Self-Occupied Property: If you live in your own property (up to two properties), no rent is taxable—GAV is nil.

- Unrealized Rent: Rent due but not received isn’t taxed if it’s legally unrecoverable (e.g., tenant defaults, and you meet Section 25A conditions).

- Business Use: Rent from property used for your own business isn’t taxed under this head.

Calculating Income From House Property

Steps For Computations Of Income From House Property For Let Out Property. There are some simple steps you need to follow to make the calculation of the income of the house property.

Step 1: Determine the Gross Annual Value (GAV)

- The GAV is the potential rental income from the property.

- Calculate Actual Rent Received or Receivable:

- Total rent due or collected from the tenant for the year.

- Subtract unrealized rent (rent not received) only if it’s legally unrecoverable under Section 25A conditions:

- Tenant has vacated or steps taken to evict.

- Legal action initiated or rent written off as bad debt.

- No other property benefit received from the tenant.

-

Calculate Expected Rent:

- Municipal Valuation: Value assigned by local authorities for property tax.

- Fair Rental Value (FRV): Market rent for similar properties in the locality.

- Standard Rent: Maximum rent permissible under Rent Control Acts (if applicable).

- Expected Rent = Higher of Municipal Valuation or FRV, but capped by Standard Rent.

-

Determine GAV:

- GAV = Higher of Actual Rent or Expected Rent.

- Exception: If the property was vacant for part of the year (despite efforts to rent it), GAV = Actual Rent Received for the occupied period.

Example:

- Actual rent: ₹25,000/month = ₹3,00,000/year.

- Unrealized rent (unrecoverable): ₹25,000.

- Adjusted actual rent = ₹2,75,000.

- Municipal value: ₹2,80,000.

- Fair rent: ₹3,10,000.

- Standard rent: ₹3,00,000.

- Expected Rent = ₹3,00,000 (higher of municipal/fair, capped by standard).

- GAV = ₹3,00,000 (higher of ₹2,75,000 vs. ₹3,00,000).

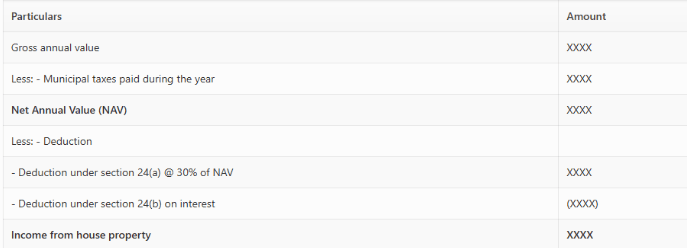

Step 2: Compute The Net Annual Value (NAV)

- Deduct Municipal Taxes:

- Subtract municipal taxes (e.g., property tax) paid by the owner during the financial year from the GAV.

- Taxes paid by the tenant or unpaid taxes don’t qualify.

- NAV Formula:

- NAV = GAV – Municipal Taxes Paid.

Example:

- GAV = ₹3,00,000.

- Municipal tax paid: ₹20,000.

- NAV = ₹3,00,000 – ₹20,000 = ₹2,80,000.

Step 3: Apply Deductions under Section 24

- Two deductions are allowed from NAV to arrive at taxable income:

- Standard Deduction:

- 30% of NAV, regardless of actual expenses on repairs, maintenance, or other costs.

- This is a fixed allowance under Section 24(a).

- Interest on Borrowed Capital:

- Interest paid on a loan taken for acquisition, construction, repair, renewal, or reconstruction of the property under Section 24(b).

- For let-out properties, there’s no upper limit on this deduction (unlike self-occupied properties, capped at ₹2,00,000).

- Pre-construction interest (before completion) is deductible in 5 equal annual installments starting from the year of completion.

Example:

- NAV = ₹2,80,000.

- Standard deduction (30%) = 0.30 × ₹2,80,000 = ₹84,000.

- Loan interest paid: ₹1,50,000.

- Total deductions = ₹84,000 + ₹1,50,000 = ₹2,34,000.

Step 4: Calculate Taxable Income From House Property

-

Formula:

- Taxable Income = NAV – (Standard Deduction + Interest on Borrowed Capital).

- If deductions exceed NAV, it results in a loss under this head, which can be:

- Set off against other income (e.g., salary) up to ₹2,00,000 in the same year.

- Carried forward for up to 8 years to offset future house property income.

Example:

- NAV = ₹2,80,000.

- Total deductions = ₹2,34,000.

- Taxable Income = ₹2,80,000 – ₹2,34,000 = ₹46,000.

Loss Example:

- NAV = ₹2,80,000.

- Interest = ₹3,50,000.

- Standard deduction = ₹84,000.

- Total deductions = ₹4,34,000.

- Taxable Income = ₹2,80,000 – ₹4,34,000 = -₹1,54,000 (loss).

House Property Income Calculation Chart

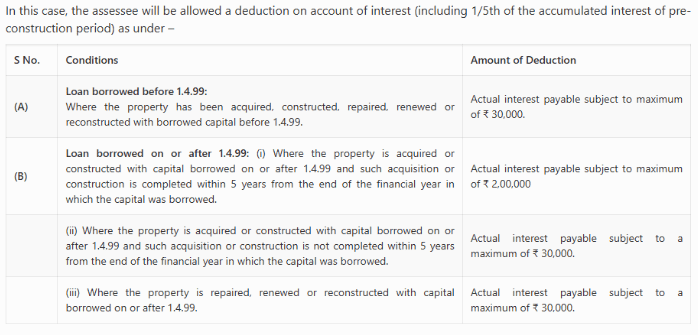

Deduction In Respect To House Property Where Annual Value Is Nil

Final Take Away

Hence, these are some of the core concepts from income from House Property that you must be well aware of. Computation of the house property can be complex at times as its tax slabs keep on changing from time to time.

You can share your opinions and views in our comment box. This will help us to know your take on this matter. Once you follow the correct process things will become easier for you in the long run.